The most recognized cryptocurrency is Bitcoin.

Bitcoin was introduced in 2009, following the release of a report detailing the Bitcoin system under the pseudonym Satoshi Nakamoto. The system was crafted to electronically replicate the characteristics of a cash transaction. It was intended to facilitate peer-to-peer (or person-to-person) transactions, eliminating the necessity to know or trust the other party involved, and to function without a central authority (like a bank).

In contrast to traditional national currencies such as the Australian dollar, which derive part of their value from being designated as legal tender, Bitcoin and other cryptocurrencies lack any legislated or inherent value. Instead, Bitcoin's worth is dictated by what individuals are prepared to pay for it in the marketplace (and theoretically, its value could plummet to zero at any moment).

A notable aspect of the Bitcoin system is that the supply of Bitcoins grows at a predetermined rate and is limited to approximately 21 million (with each bitcoin capable of being divided into 100 million satoshis or 0.00000001 bitcoins). Consequently, the supply of Bitcoins is often likened to that of a limited resource, such as gold.

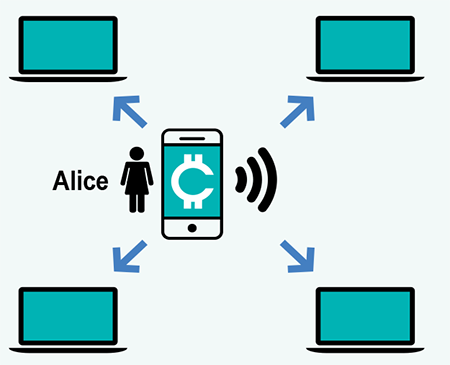

The Bitcoin system enables transactions to take place directly between individuals without the need for a central authority (like a bank) to authenticate or document the transactions. This contrasts with most traditional payment methods, such as electronic bank transfers, which depend on a central entity to maintain and update transaction records. For instance, commercial banks keep a record of their clients' account balances, deposits, and withdrawals.

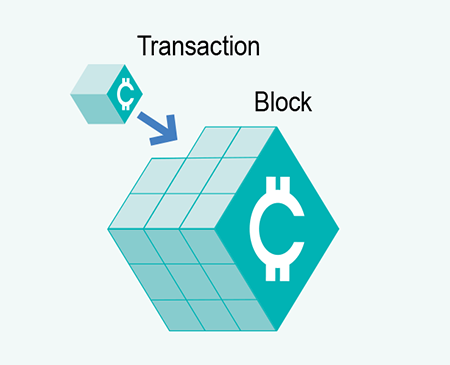

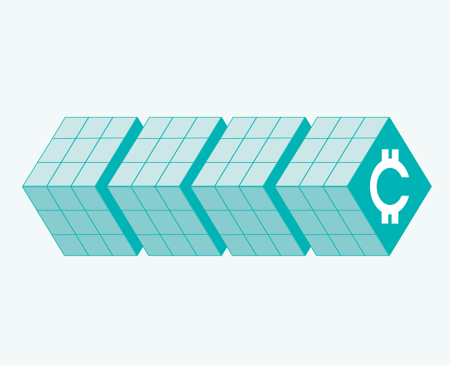

Instead, the Bitcoin network utilizes ‘blockchain’ technology to document transactions and the ownership of bitcoins. This technology essentially links groups of transactions (‘blocks’) together over time (forming a ‘chain’). Each time a transaction takes place, it becomes part of a new block that is appended to the chain. Consequently, the blockchain serves as a record (or database) of every bitcoin transaction that has ever taken place, accessible for anyone to view and update on a public network (commonly known as a ‘distributed ledger’). The security of the Bitcoin system is upheld by ‘cryptography’, a technique for verifying and safeguarding data through intricate mathematical algorithms (or codes). This renders the system extremely resistant to corruption.

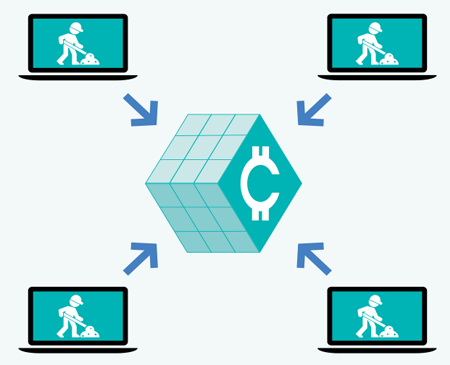

Bitcoin transactions are validated by other users within the network, and the process of assembling, verifying, and confirming transactions is frequently termed ‘mining’. Specifically, intricate codes must be solved to validate transactions and ensure the system remains uncorrupted. The Bitcoin system escalates the complexity of these codes as additional computing power is employed to resolve them. A new block of transactions is generated approximately every ten minutes. ‘Miners’ are motivated to solve these codes and process transactions because they receive rewards in the form of new bitcoins (currently 6.25 new Bitcoins per block).

The rising competition among miners for new Bitcoins has led to significant increases in the amount of computing power and electricity needed (often utilized for air conditioning to cool computer systems). Although precise calculations are challenging, some estimates indicate that the annual energy consumption of the Bitcoin system is roughly equivalent to that of the country of Thailand.

This explainer aims to enhance your understanding of cryptocurrencies. It should not be interpreted as advice or a recommendation to purchase, trade, or invest in Bitcoin or any other cryptocurrency. Should you choose to trade or utilize cryptocurrencies, be aware that you may be assuming risks for which there is no remedy.